Government Securities (G-Secs): The Safest Investment in India?

The world of investments is often seen as a trade-off between risk and reward. But in the Indian financial landscape, one asset class stands alone, promising the ultimate safety: Government Securities (G-Secs).

Commonly referred to as government bonds, these instruments are considered the bedrock of the country’s debt market. But are they truly the “safest” investment, and how can an everyday retail investor access them today? Let’s dive into the core of G-Secs, their hidden risks, and the modern investment process.

1. What Exactly are Government Securities (G-Secs)?

Government Securities India (G-Secs) are debt instruments issued by the Central or State Governments to borrow money from the public to meet their financial requirements, such as funding infrastructure projects or bridging fiscal deficits.

The fundamental assurance that makes them unique is the Sovereign Guarantee. Since they are backed by the issuing government, the chance of the borrower defaulting (credit risk) is considered virtually zero.

Types of G-Secs

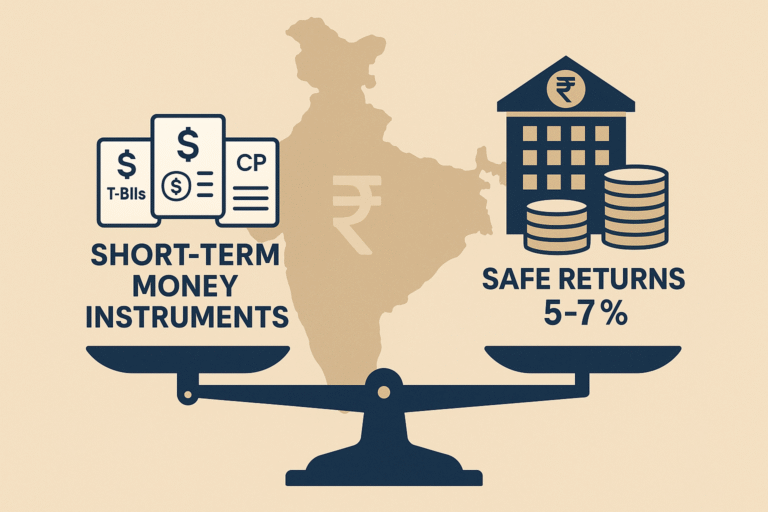

G-Secs come primarily in two forms:

- Treasury Bills (T-Bills): Short-term instruments with maturities of 91, 182, or 364 days. T-Bills do not pay interest; they are issued at a discount to their face value and redeemed at par.

- Dated Securities (Bonds): Long-term instruments with maturities ranging from 5 to 40 years. These pay a fixed or floating interest rate, known as the coupon, semi-annually.

- State Development Loans (SDLs): Bonds issued by individual State Governments. While still highly secure, they are benchmarked slightly below Central Government Securities.

2. The Case for Absolute Safety (Zero Default Risk)

The title question asks if G-Secs are the safest, and in one crucial area, the answer is a resounding Yes.

- Zero Credit Risk: Unlike corporate bonds, where the company might go bankrupt, a sovereign government has the power to raise money through taxation or currency printing. This means the risk of the government failing to pay the interest (coupon) or the principal upon maturity is negligible. This is why G-Secs are the benchmark for all other debt instruments.

- Liquidity: Central Government Securities India are highly liquid. They are actively traded on the secondary market (BSE and NSE), allowing investors to buy or sell them relatively easily before maturity.

3. The Reality Check: The Risks You MUST Understand

While G-Secs carry zero default risk, they are not risk-free. The following market risks are critical to understand, especially for long-term bonds:

A. Interest Rate Risk (The Biggest Risk)

This is the primary risk for bondholders who might need to sell their bonds before maturity.

- Inverse Relationship: When the prevailing interest rates in the economy rise, the market price of your older G-Secs (which offer a lower, fixed coupon rate) falls.

- Impact: If you are forced to sell a long-term bond when interest rates are high, you could suffer a capital loss. This risk is nullified only if you hold the G-Sec till its maturity date.

B. Inflation Risk (The Real Return Killer)

- G-Secs provide a fixed coupon rate. If the rate of inflation exceeds the coupon rate of your bond, the purchasing power of your interest income and your principal repayment is eroded. In this scenario, your real return is negative.

4. G-Secs vs. Bank Fixed Deposits (FDs): A Quick Comparison

For the average retail investor, G-Secs are often compared to bank FDs. Here is the key difference, especially regarding risk:

| Feature | Government Securities (G-Secs) | Bank Fixed Deposits (FDs) |

| Credit Risk | Zero (Sovereign Guarantee) | Very Low (Insured up to ₹5 Lakh per bank by DICGC) |

| Interest Rate Risk | High (Price changes with market rates) | Minimal (Principal is not marked-to-market) |

| Liquidity | High (Tradable on stock exchange) | Low (Premature withdrawal penalty applies) |

| Taxation | Interest is fully taxable. Capital Gains Tax on price appreciation (if sold). | Interest is fully taxable (TDS applies). |

Verdict: G-Secs offer ultimate credit safety and better liquidity, but FDs offer better safety from interest rate volatility.

5. How Retail Investors Can Buy Government Securities India (The Modern Way)

Historically difficult to access, G-Secs are now simple to buy, thanks to the Reserve Bank of India (RBI).

1. The RBI Retail Direct Scheme (Recommended)

Launched by the RBI, this platform allows individual investors to directly open a free Retail Direct Gilt (RDG) Account with the RBI.

- Process: Register on the RBI portal, complete KYC, and link your bank account.

- Benefit: Allows direct participation in the primary auctions (buying new issues directly from the government) and trading in the secondary market.

2. Through Demat Accounts

You can buy and sell G-Secs using your existing Demat and Trading accounts via platforms like NSE goBID.

- Process: Your broker acts as an intermediary to submit your bids during the auction window.

3. Via Gilt Mutual Funds

For passive investors, Gilt Mutual Funds and Gilt ETFs offer an indirect and diversified way to invest in a portfolio of Government Securities India, managed by professionals.

Final Verdict: Is a G-Sec Investment Right for You?

G-Secs are the safest investment in India in terms of capital protection (default risk).

They are an excellent fit for:

- The Ultra-Conservative Investor: Those prioritizing preservation over maximum return.

- Long-Term Goal Savers: Investors who can hold the bond until maturity (e.g., retirement corpus, long-term education fund), thereby neutralizing the interest rate risk.

- Portfolio Diversification: They act as the perfect low-risk anchor to balance the volatility of high-risk assets like stocks.

If your primary need is safety, G-Secs should certainly be a core component of your long-term investment strategy.