Your Global Financial Lifeline: A Comprehensive Guide to Building and Maintaining an Emergency Fund for Any Life Scenario

Imagine This…

You’re going about your life, making plans, building dreams. Then, without warning, the ground shifts. You lose your job unexpectedly in a global economic downturn. A loved one across the world needs urgent, uninsured medical care. Or perhaps, your landlord suddenly hikes the rent, and you’re left scrambling for solutions. These moments don’t ask where you live, how much you earn, or what your aspirations are. They just hit. And for many, they can unravel years of hard work and peace of mind if they’re unprepared.

That’s precisely where an emergency fund steps in. It’s not just a number on a bank statement; it’s your shield against the unexpected, your source of calm in chaos, your indispensable financial first aid kit. This ultimate guide from CrunchyFin is your clear, actionable roadmap to understanding, building, and protecting that vital fund empowering you regardless of your location, income level, or the challenges life throws your way.

What Exactly is an Emergency Fund? Your Undefined Financial Guardian

At its core, an emergency fund is a dedicated financial buffer designed solely for urgent, unforeseen needs. Think of it as a separate pool of money set aside specifically to handle life’s inevitable curveballs. Its sole purpose is to provide a safety net when a true crisis strikes, preventing you from sinking into debt or derailing your long-term financial goals.

Crucially, an emergency fund is distinct from your other savings goals. It is not for that dream vacation you’re planning, the latest gadget you’ve been eyeing, or taking advantage of a seasonal sale. Dipping into your emergency fund for anything less than a genuine crisis defeats its entire purpose, leaving you vulnerable when a true financial fire erupts. To visualize its role, think of it as your financial oxygen mask, ready to deploy when life’s cabin pressure drops unexpectedly, or perhaps your spare tire on a long journey, there only for those essential, unexpected punctures.

Why This Financial Safety Net is Non-Negotiable in Our Connected World

In today’s interconnected global landscape, financial stability can feel more elusive than ever. An emergency fund isn’t just a good idea; it’s a fundamental necessity for everyone.

- Global Economic Volatility: From sudden industry shifts to worldwide economic slowdowns, job security is increasingly less predictable. Losing an income source can quickly become catastrophic without a buffer.

- Skyrocketing Costs: Across continents, the cost of living be it housing, healthcare, education, or even basic utilities continues its relentless climb. An emergency fund helps absorb these inevitable shocks, protecting your existing financial stability.

- Unforeseen Life Events: Life is unpredictable. Accidents happen. Illnesses strike. Natural disasters can devastate. A global pandemic taught us that unforeseen events can impact everyone, everywhere, demanding immediate financial resilience.

- Debt Trap Prevention: Without a dedicated emergency fund, a seemingly minor car repair or an unexpected medical bill can quickly force you into high-interest debt whether it’s a credit card spiral or a desperate payday loan. Your emergency fund acts as a crucial barrier, protecting your hard-earned money from predatory interest rates and the stress of mounting debt.

- A Priceless Mental Health Booster: Beyond the numbers, the true value of an emergency fund lies in the profound peace of mind it offers. Knowing you have a buffer against the unknown significantly reduces anxiety, improves decision-making during stressful times, and allows you to focus on building a better future, rather than constantly worrying about the next financial blow.

How Much is Truly Enough? Customizing Your Fund for Your Unique Life

So, the big question on everyone’s mind is, “How much money do I actually need?” While there’s no single magic number that fits every person across every continent, a widely accepted rule of thumb provides a powerful starting point: aim for 3 to 6 months of your essential living expenses.

However, your ideal amount is a deeply personal calculation, adapting to your unique circumstances and the economic realities of your region. Consider these crucial factors:

- Your Job Security: If your employment is less stable (e.g., freelance, contract work, or in an industry prone to economic swings), aiming for 6 to 12 months or even more might offer greater peace of mind. Conversely, someone with an extremely secure, stable job might feel comfortable with closer to three months.

- Number of Dependents: More mouths to feed or individuals relying on your income means a larger buffer is prudent. Your fund needs to cover the basic needs of everyone under your financial care.

- Local Healthcare System & Social Safety Nets: Consider the healthcare system in your country. In regions with significant out-of-pocket medical costs or where insurance is less comprehensive, a larger fund for potential medical emergencies is wise. Similarly, if your country has minimal unemployment benefits or social support systems, your fund needs to cover a longer period of income loss.

- Fixed vs. Variable Living Costs: Distinguish between your fixed, non-negotiable expenses (rent/mortgage, basic utilities, essential food, core transportation) and your variable, discretionary spending (entertainment, dining out, luxury items). Your emergency fund should cover the absolute minimum needed to survive, not your entire lifestyle.

- Career Stability and Country Mobility: If your career is volatile, or you anticipate potential international relocation (which often involves unexpected costs), these factors might warrant a higher fund.

Your Actionable Step: Start by meticulously calculating your absolute minimum monthly expenses. This might include rent/mortgage, basic utilities, food, essential transportation, and basic insurance premiums. Multiply that by your chosen number of months (3, 6, or more) to arrive at your personal emergency fund target. A simple expense tracker or spreadsheet can be invaluable here.

The Starting Line: Building a Fund When You Feel Like You Have Nothing

For many, the idea of saving thousands seems impossible, especially if you’re living paycheck-to-paycheck or carrying debt. If this sounds like you, remember: You are not alone. Most of the world faces financial constraints, but every financial journey begins with a single, small step.

- The Power of the “Starter Fund”: Instead of aiming for the full amount immediately, focus on a smaller, achievable goal first. This “starter fund” whether it’s enough for one month’s rent, $500, ₹5000, or a specific local currency equivalent acts as an immediate psychological win and a crucial barrier against minor financial setbacks. It builds momentum and proves to yourself that you can save.

- Navigating Debt: Strategic Prioritization: If you’re grappling with high-interest debt (like credit card debt or payday loans), a common dilemma arises: pay off debt or build the fund? The general consensus is to save your small starter fund first. This provides a basic cushion for immediate crises. Then, aggressively tackle your high-interest debt. Once that urgent debt is under control, you can then redirect those freed-up funds towards completing your full emergency fund. It’s a phased approach designed for real-world scenarios.

- Grow Steadily, Sustainably: Once your urgent, high-interest debt is under control, the money you were using for payments can now be consistently directed towards growing your emergency fund. This isn’t a race; it’s about building sustainable habits.

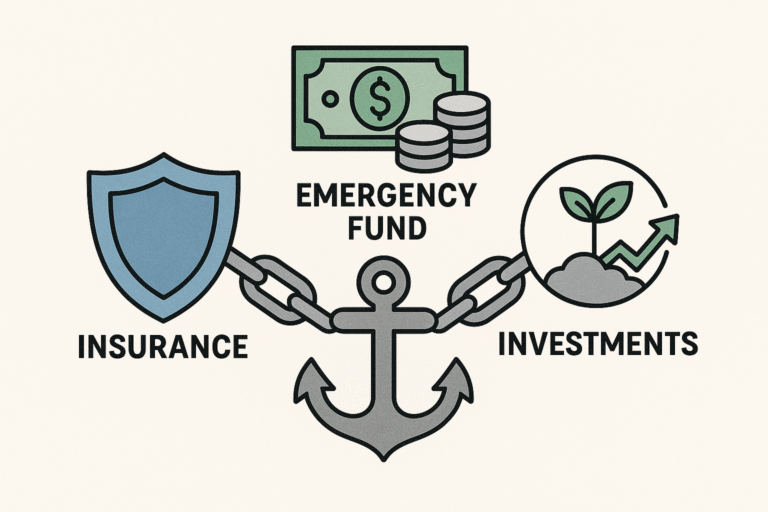

Where Your Financial Guardian Should Reside: Safety, Liquidity, & Separation

Once you start saving, where should you keep your emergency fund? The location is as important as the amount. Your fund must adhere to three golden rules:

- Safety of Principal: Your emergency fund must be protected from market fluctuations. This means no exposure to volatile assets like stocks, cryptocurrencies, or speculative investments. Its primary purpose is safety and preservation of your capital, not aggressive growth.

- High Liquidity: You need immediate, unhindered access to these funds without penalties or significant delays. An emergency won’t wait for your investments to mature or for a withdrawal process to clear over several days.

- Separation: Keep your emergency fund in an account separate from your daily spending and bill-paying accounts. This creates a crucial psychological barrier, making it harder to dip into it for non-emergencies and fostering a clear sense of dedicated purpose.

Best Options Globally :

- High-Yield Savings Accounts (HYSAs): These accounts generally offer better interest rates than standard savings accounts while maintaining high liquidity. It’s important to note that their availability, interest rates, and specific features will vary significantly by country and financial institution. Always research options available in your local market.

- Money Market Accounts: Similar to HYSAs, these often offer competitive interest rates and, in some regions, may even provide limited check-writing capabilities.

- Short-Term Fixed Deposits / Certificates of Deposit (CDs): For a portion of a larger emergency fund, some individuals might consider short-term fixed deposits or CDs that have minimal or no penalties for early withdrawal. Ensure you fully understand the terms and conditions in your region regarding access.

- Liquid Mutual Funds / Overnight Funds: These are generally low-risk funds designed for liquidity. However, it’s vital to understand that any investment carries some market risk, and settlement times (how long it takes for money to reach your bank account after redemption) can vary. For a global audience, this option should be approached with caution and always with a strong recommendation to consult a local, licensed financial professional for guidance on specific products suitable for your region and risk tolerance.

What to Absolutely AVOID:

To reiterate: Your emergency fund should never be tied up in volatile assets like stocks, cryptocurrencies, or illiquid assets such as real estate. These are powerful tools for long-term wealth building, but they are entirely unsuitable for your immediate crisis protection.

How to Actually Build It: Actionable Strategies for Any Income Level

The good news is that building an emergency fund is achievable for anyone, regardless of income, through consistent habits and smart strategies.

- Automate Your Savings: This is the simplest yet most powerful strategy. Set up a recurring transfer (weekly, bi-weekly, or monthly) from your main account to your dedicated emergency fund. This removes the need for willpower and ensures consistency. “Set it and forget it” genuinely works.

- “Pay Yourself First”: Treat your emergency fund contribution like a non-negotiable bill. Before you pay rent, groceries, or entertainment, pay your future self. This simple mindset shift prioritizes your financial security and prevents you from finding excuses.

- Harnessing Windfalls: Unexpected money a work bonus, a tax refund, a gift, or even a small lottery win—should be directly funneled into your emergency fund. These “found” monies accelerate your progress dramatically without impacting your regular budget.

- Strategic Expense Reduction: Take a hard, honest look at your spending. Can you cut unused subscriptions? Cook at home more often instead of eating out? Find free entertainment options? Even small, consistent cuts accumulate quickly. Every penny saved is a penny earned for your fund.

- Boosting Your Income (If Possible): Consider ways to earn extra income specifically for your emergency fund. This could involve selling items you no longer need, taking on a temporary side gig, or offering a skill-based service. Every extra bit helps accelerate your goal.

- The Motivation of Progress: Visually track your progress. Use a spreadsheet, a budgeting app, or even a simple chart on your wall. Seeing your fund grow, even by small increments, provides immense motivation and reinforces your positive habits. Celebrate each milestone!

The Layered Emergency Fund Approach: Advanced Resilience for Complex Lives

For some, particularly those with highly variable incomes (like freelancers or business owners), significant dependents, or unique vulnerabilities, a single 3-6 month lump sum might not feel sufficient. This is where a “layered” approach can provide even greater peace of mind and strategic access.

- Tier 1: The Immediate Cash Cushion (1-2 weeks of essentials). This small amount should be ultra-accessible, perhaps in your regular checking account or a very easily transferable savings account. Its purpose is to cover tiny, urgent surprises (e.g., a small unexpected repair, a minor utility bill) without touching your main emergency fund.

- Tier 2: The Core Safety Net (3-6 months of essentials). This is the primary fund, ideally held in a high-yield savings account or equivalent. It’s designed for major life events like job loss, significant medical bills, or substantial unexpected home/car repairs.

- Tier 3: The Contingency Buffer (6-12+ months or more). For those with higher risk profiles (e.g., self-employed individuals with unpredictable income, or if you’re saving for a very specific, high-cost potential emergency like long-term care), consider building this larger buffer in slightly less liquid, but still very safe, vehicles like short-term fixed deposits or ultra-low-risk, highly liquid bond funds (again, with necessary local professional consultation).

When to Deploy Your Lifeline (and How to Rebuild It Stronger)

Your emergency fund is sacred, but it’s meant to be used. The key is to distinguish between a true emergency and a mere desire.

- Use ONLY for True Emergencies: Your fund is for situations that are: 1) Unexpected (not a planned expense), 2) Necessary (not a want), and 3) Urgent (requires immediate attention). Think:

- Job loss or significant income reduction.

- Emergency medical bills or urgent healthcare needs.

- Major, unforeseen car or home repairs essential for safety/living.

- Critical, unplanned family needs (e.g., emergency travel).

- Not For: Conversely, your emergency fund is not for a fantastic flight sale, the latest smartphone, a spontaneous vacation, or that designer outfit you’ve been eyeing. Resist the temptation to redefine “emergency” to fit a want. Using it for non-emergencies undermines its purpose and leaves you vulnerable when a real crisis strikes.

- The Crucial Refill Plan: If you dip into your fund, the very next step is to prioritize its replenishment. Treat it like the most important loan you’ll ever repay a loan to your future self.

- Pause Extras: Temporarily halt discretionary spending (subscriptions, wants).

- Redirect Income: Funnel any extra income, bonuses, or windfalls directly back into the fund.

- Adjust Budget: Reassess your budget to find areas where you can temporarily cut back to rebuild your buffer quickly.

Facing the Emotional Blocks: Turning Financial Anxiety into Action

Building an emergency fund isn’t just about numbers; it’s about navigating universal human emotions like fear, procrastination, and overwhelm. These feelings are common, but so are the strategies to overcome them.

- “I can’t afford to save.” This is perhaps the most common belief. But saving isn’t about the amount; it’s about the habit and starting. Begin with literally a single coin, or the smallest denomination you can spare. Consistency, even in tiny amounts, builds momentum and changes your mindset from “I can’t” to “I can.”

- “I always dip into it.” The solution lies in making it harder to access. Use a separate bank account that isn’t linked to your daily spending. Hide the debit card for that account. Automate transfers so you don’t even see the money—this creates a psychological barrier, making it much harder to use for non-emergencies.

- “I’m overwhelmed; it feels impossible.” Break the goal into tiny, manageable pieces. Focus on saving just $50 this month, then $100 next month. You don’t need the full fund overnight. Celebrate each small milestone. Remember: progress, not perfection, is the goal.

- “Inflation will eat my savings.” This is a valid concern for long-term wealth, but your emergency fund is a safety net, not a growth investment. Its primary purpose is capital preservation and liquidity, ensuring the money is there when you need it. While inflation is a real concern for long-term wealth, your emergency fund’s immediate purpose is crisis prevention. Once your emergency fund is fully funded and maintained, then you can focus on building investment accounts to outpace inflation and grow your wealth.

- “I rely on family/community in emergencies.” This is a beautiful and vital aspect of many cultures worldwide. However, imagine the strength and dignity you gain by being able to handle your own immediate crises, or even contribute to community needs without added personal burden. A personal safety net empowers you to help yourself and others more effectively, complementing existing support systems.

The Bigger Picture: Why It Changes Lives (Beyond the Bank Balance)

Building an emergency fund transcends mere financial planning; it’s a transformative act that impacts every area of your life.

- Freedom and Choice: An emergency fund is not just money; it’s freedom. It’s the ability to say “no” to a toxic job, “no” to predatory loans, and “yes” to unexpected opportunities you might otherwise miss. It empowers you to make decisions from a place of strength, not desperation.

- Reduced Stress & Improved Well-being: The peace of mind an emergency fund provides is invaluable. It significantly reduces financial anxiety, improves sleep, and frees up valuable mental energy. You’re no longer operating in constant survival mode, allowing you to focus on personal growth, pursuing dreams, and genuine well-being.

- Goal Acceleration: Knowing your emergency needs are covered prevents unexpected setbacks from derailing your long-term goals, whether it’s buying a home, funding education, or investing for retirement.

- A Legacy of Preparedness: By building your own financial lifeline, you’re not just securing your future; you’re setting a powerful example. You’re teaching your children, inspiring your community, and demonstrating the profound value of proactive financial responsibility for generations to come.

Your Next Step: Take Action Today

The journey to financial resilience begins with a single, deliberate step. Don’t wait for a crisis to strike—start building your shield today.

- Open a dedicated savings account JUST for emergencies. Keep it separate from your daily banking.

- Move even a small amount ₹100, $1, €5, or whatever feels achievable into that account right now. Consistency trumps quantity in the beginning.

- Identify one non-essential expense from your last month’s spending and commit to cutting it. Redirect that money immediately into your new emergency fund.

- Share this guide with someone you care about who might need this lifeline. Empowering others is part of building a resilient global community.

You don’t need to be rich to build a safety net. You just need to start. And CrunchyFin is here to walk with you every step of the way.

FAQs

- What is the primary purpose of an emergency fund?

To cover unexpected, urgent expenses without going into debt. - How much should I save in my emergency fund?

Aim for 3–6 months of essential expenses, customizing based on your job security, dependents, and local economic conditions. - Where is the best place to keep my emergency fund?

A high-yield savings account or equivalent—it must be safe, highly liquid, and separate from your daily spending. - Can I invest my emergency fund?

No. Emergency funds should not be exposed to market risk; their priority is safety and immediate accessibility. - What if I need to use it?

Use it—that’s what it’s for! But make a plan to start refilling it immediately after. - How do I build one if I’m on a tight budget?

Start small, even with tiny amounts. Save a little regularly. Cut unnecessary costs. Increase income when possible and dedicate windfalls.

Remember: This isn’t just about money. It’s about taking control. Creating breathing space. Giving yourself and your future a fighting chance. You deserve that. And we’re here to help you get there.

3 Comments